{kind=link}

The name of this blog is Science-Based Medicine, because we seek to champion medicine that is based on rigorous science as the safest and most effective medicine. Before the pandemic, much of what we used to write about was the infiltration of pseudoscientific medicine and medicine based far more on prescientific or religious ideas than science, although common threads even since the pandemic remain. These include, but are not limited to, the antivaccine movement, COVID-19 minimization/denial (much like germ theory denial that undergirds a lot of alternative medicine and antivaccine beliefs), resistance to public health measures, and, of course, the promotion of quackery, in the case of the pandemic (among many other things) the promotion of drugs that were unproven but are now disproven as effective treatments for COVID-19; i.e., ivermectin, hydroxychloroquine, and others.

However, there’s more to SBM than rigorous basic and clinical science, a Bayesian approach to evaluating evidence that considers prior plausibility based on basic science, randomized clinical trials, and epidemiology. The most effective science-based treatments will do no good if they are not available to patients who need them, for whatever reason, and this is where, unavoidably, social sciences and politics come in. I’ve long said that we at SBM are not apolitical, although we do strive to be as nonpartisan as individuals can be given their biases. After all, opposing the licensing of quacks, the continued sale of homeopathic products without the requirement by the FDA that they demonstrate safety and efficacy, and agreeing that physicians who spread medical misinformation should face sanctions from state licensing boards (for example) are far from apolitical. In some cases they aren’t even nonpartisan, given how it was prominent Democrats who championed the National Center for Complementary and Integrative Health (NCCIH) that we have long advocated dismantling, and these days the Republican Party that is promoting resistance to public health measures designed to mitigate the impact of the pandemic. That being said, SBM will never be as effective in ameliorating human suffering if public policy considerations are not taken into account and also based as much as possible in science. What that means is that SBM cannot—and I now argue, should not—avoid social science and politics. Of course, as difficult as it is to deconstruct antivaccine misinformation, various alternative medicine pseudoscience, and false claims about COVID-19, I am well aware that looking at SBM at a more macro level in which it interacts with society at large and its political and economic systems adds even more complexity to the mix, but we do need to consider these problems—and consider them more.

What got me thinking about these issues, which I had been meaning to bring up, were two news reports about studies. I listened to one of these on NPR on the way to work on Thursday morning, a story about how 100 million people in the US live with medical debt (based on the KFF Health Care Debt Survey) that also featured brief stories about individuals who make up that figure. The second was a series of stories about a study that concluded that single payer universal health insurance (which we in the US still do not have, “Obamacare” notwithstanding) could potentially have saved hundreds of thousands of lives during the pandemic. Obviously, the two stories are related, because the cause of so much medical debt in the US is clearly the lack of universal health insurance. Many families who are uninsured or underinsured face financial catastrophe.

Medical debt: Deferring or foregoing SBM due to financial constraints

While on my way to work last Thursday, I was flipping radio stations in my car and landed on NPR, only to hear:

Elizabeth Woodruff drained her retirement account and took on three jobs after she and her husband were sued for nearly $10,000 by the New York hospital where his infected leg was amputated.

Ariane Buck, a young father in Arizona who sells health insurance, couldn’t make an appointment with his doctor for a dangerous intestinal infection because the office said he had outstanding bills.

Allyson Ward and her husband loaded up credit cards, borrowed from relatives, and delayed repaying student loans after the premature birth of their twins left them with $80,000 in debt. Ward, a nurse practitioner, took on extra nursing shifts, working days and nights.

“I wanted to be a mom,” she said. “But we had to have the money.”

The three are among more than 100 million people in America ― including 41% of adults ― beset by a health care system that is systematically pushing patients into debt on a mass scale, an investigation by KHN and NPR shows.

The investigation reveals a problem that, despite new attention from the White House and Congress, is far more pervasive than previously reported. That is because much of the debt that patients accrue is hidden as credit card balances, loans from family, or payment plans to hospitals and other medical providers.

Again, SBM can do some truly amazing things and save lives that would have been lost even a couple of decades ago. However, it can’t help if people can’t afford to access it, and it will be much less effective if people suffer such major financial consequences for having accessed it.

The number is truly staggering, given that the poll found that in the past five years, more than half of US adults report they’ve gone into debt because of medical or dental bills, with a quarter of people with health care debt owing more than $5,000 and about one in five with any amount of debt said they don’t expect ever to be able to pay it off. I’m sure that our European and Australian readers will facepalm at these findings, but they track. As the poll and news story noted, even though the Affordable Care Act (ACA) did dramatically reduce the percentage of Americans who are uninsured, an unfortunate problem with it is that a lot of the health insurance policies sold in the ACA marketplaces have high deductibles, making it very possible for less affluent people to go deeply into debt even though they ostensibly have health insurance. It’s the deductibles that get them.

Worse:

Perhaps most perversely, medical debt is blocking patients from care.

About 1 in 7 people with debt said they’ve been denied access to a hospital, doctor, or other provider because of unpaid bills, according to the poll. An even greater share ― about two-thirds ― have put off care they or a family member need because of cost.

“It’s barbaric,” said Dr. Miriam Atkins, a Georgia oncologist who, like many physicians, said she’s had patients give up treatment for fear of debt.

This last example strikes close to home, given my surgical specialty. I will admit that it’s been rare in my practice for a patient to be reluctant to undergo surgery for breast cancer. However, what is often not appreciated is that surgery is actually likely the least expensive part of the multidisciplinary care of this disease. Totalled up, the chemotherapy tends to cost a lot more, particularly when newer drugs are used, such as immune checkpoint inhibitors or the newer HER2-blocking drugs.

Indeed, the story includes the example of Cheyenne Dantona, who is now 31 but was diagnosed with a blood cancer while in college:

The cancer went into remission, but when Dantona changed health plans, she was hit with thousands of dollars of medical bills because one of her primary providers was out of network.

She enrolled in a medical credit card, only to get stuck paying even more in interest. Other bills went to collections, dragging down her credit score. Dantona still dreams of working with injured and orphaned wild animals, but she’s been forced to move back in with her mother outside Minneapolis.

“She’s been trapped,” said Dantona’s sister, Desiree. “Her life is on pause.”

Desiree Dantona said the debt has also made her sister hesitant to seek care to ensure her cancer remains in remission.

Another example:

Sherrie Foy, 63, and her husband, Michael, saw their carefully planned retirement upended when Foy’s colon had to be removed.

After Michael retired from Consolidated Edison in New York, the couple moved to rural southwestern Virginia. Sherrie had the space to care for rescued horses.

The couple had diligently saved. And they had retiree health insurance through Con Edison. But Sherrie’s surgery led to numerous complications, months in the hospital, and medical bills that passed the $1 million cap on the couple’s health plan.

When Foy couldn’t pay more than $775,000 she owed the University of Virginia Health System, the medical center sued, a once common practice that the university said it has reined in. The couple declared bankruptcy.

The Foys cashed in a life insurance policy to pay a bankruptcy lawyer and liquidated savings accounts the couple had set up for their grandchildren.

Most oncologists who practice in areas like Detroit (where I practice) have observed this phenomenon firsthand. I daresay that even oncologists who practice in more affluent areas have also seen it.

One aspect of this problem not included in the story because it is not about patients’ debt is the massive infrastructure devoted by insurance companies to prior authorizations. Again, prior authorization is a concept foreign to many other nations and refers to the requirement by an insurance company that it authorize a proposed treatment before that treatment can be undertaken and reimbursed. Failure to get prior authorization will usually mean that the insurance company won’t pay for it; so providers’ offices and hospitals are very careful to obtain prior authorization to begin treatment. Unfortunately, as known by any physician, NP, or nurse who has to deal with insurance companies’ prior authorization departments, obtaining prior authorizations can quickly descend into truly Orwellian depths of language denying them. The process is so bad that it’s often lampooned in cartoons and videos, for example, the ever-amusing Dr. Glaucomflecken.

Lest you think that the good doctor is exaggerating, I included a response with a video of an actual prior authorization call:

real life https://t.co/lOjmW6c0IN

— Amy Walsh, 〽️D (@doctordirectmd) June 16, 2022

Given how difficult and bureaucratic the entire approach to prior authorizations has become, hospitals now have significant infrastructure devoted just to prior authorizations, and small, private practice offices end up devoting ridiculous amounts of time that could be devoted to patient care just trying to make sure they can be paid for their services. I won’t dwell on this any more—nor will I even mention it again in this post—because our inconvenience as physicians dealing with insurance company bureaucracy pales in contrast to the suffering of patients who have difficulty accessing care or face the specter of going into major debt if they become ill. I merely mention it briefly to bolster the point that the current health insurance system in the US is designed not to facilitate SBM care, but to profit, and one way to profit is to deny more expensive care whenever possible. (Thus endeth the whining about this.)

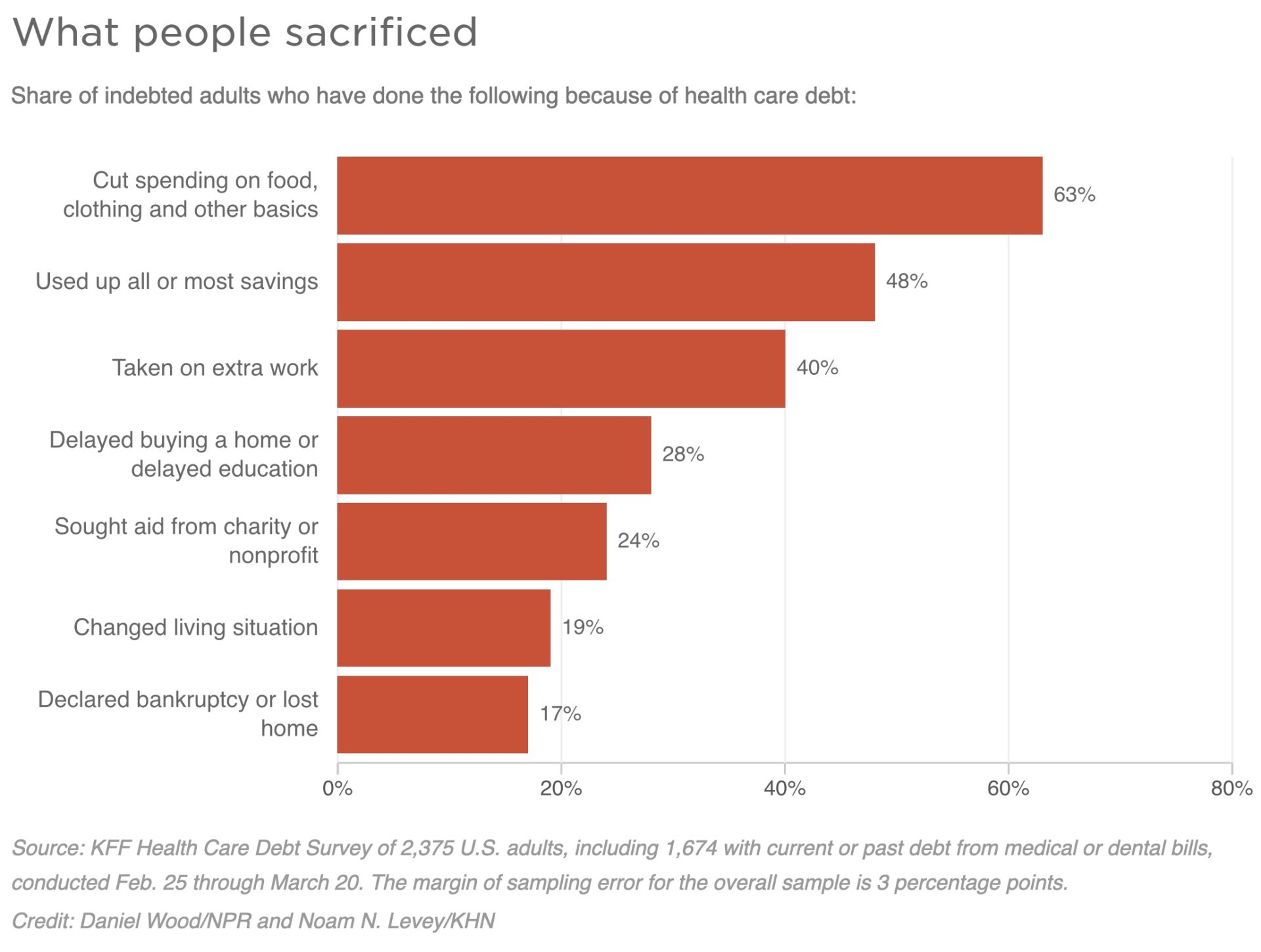

To get an idea of what people give up because of medical debt, here’s a graph included with the story:

What people forego because of medical debt in the US.

In addition:

But the medical debt on credit reports represents only a fraction of the money that Americans owe for health care, the KHN-NPR investigation shows.

- About 50 million adults ― roughly 1 in 5 ― are paying off bills for their own care or a family member’s through an installment plan with a hospital or other provider, the KFF poll found. Such debt arrangements don’t appear on credit reports unless a patient stops paying.

- One in 10 owe money to a friend or family member who covered their medical or dental bills, another form of borrowing not customarily measured.

- Still more debt ends up on credit cards, as patients charge their bills and run up balances, piling high interest rates on top of what they owe for care. About 1 in 6 adults are paying off a medical or dental bill they put on a card.

Not only is the current system apparently designed to slow or deny SBM care, it is also a medical debt machine. In fact, one thing that I hadn’t appreciated that was reported in this story is how medical debt has become big business in the US. The story first notes that in the past, medical debt on this scale was unheard of because of two reasons. First, in the past doctors and hospitals often made informal arrangements for patients to pay off medical debts; for example in the 19th century male patients at New York’s Bellevue Hospital had to ferry passengers on the East River and new mothers had to scrub floors to pay their debts. Second, and more importantly, physicians often wrote off debts that patients couldn’t afford to pay, as historian Jonathan Engel was quoted saying, “There was no notion of being in medical arrears.”

Now, efforts to collect often have horrific effects:

Edy Adams, a 31-year-old medical student in Texas, was pursued by debt collectors for years for a medical exam she received after she was sexually assaulted.

Adams had recently graduated from college and was living in Chicago.

Police never found the perpetrator. But two years after the attack, Adams started getting calls from collectors saying she owed $130.58.

Illinois law prohibits billing victims for such tests. But no matter how many times Adams explained the error, the calls kept coming, each forcing her, she said, to relive the worst day of her life.

This sort of horror is the result of a system that has sprung up that makes medical debt—and collection of that debt—big business. It’s a business that hospitals, including university hospitals and nonprofits, now partake of:

Now, a highly lucrative industry is capitalizing on patients’ inability to pay. Hospitals and other medical providers are pushing millions into credit cards and other loans. These stick patients with high interest rates while generating profits for the lenders that top 29%, according to research firm IBISWorld.

Patient debt is also sustaining a shadowy collections business fed by hospitals ― including public university systems and nonprofits granted tax breaks to serve their communities ― that sell debt in private deals to collections companies that, in turn, pursue patients.

“People are getting harassed at all hours of the day. Many come to us with no idea where the debt came from,” said Eric Zell, a supervising attorney at the Legal Aid Society of Cleveland. “It seems to be an epidemic.”

I realize that some of our readers might be unhappy that I ventured into this territory or maybe think that it is an inappropriate subject for SBM. I’m also sure that someone will be unhappy that I didn’t include their favorite issue with our healthcare system as currently constituted (e.g, for-profit big pharma companies distorting clinical trial results and driving up costs). Fair enough, but that is not the topic for today. Maybe in the future.

In the meantime, I understand, but now disagree that considering the more “meta” issues of how a political system regulates and provides SBM to its citizens is any less of a topic for this blog than discussing why the latest trial for homeopathy is bogus. Over the last few years I’ve increasingly realized that, as fantastic as SBM is at alleviating suffering, saving lives, and restoring health, it’s no good if people can’t access it without worrying about being bankrupted or incurring debts that that take years to pay off. Moreover, guess who is most affected by medical debt? While the story does note that nearly half of households making $90,000 or more a year have incurred medical debt in the last five years, it also notes that it is the poor and disadvantaged who most fall prey to this system and suffer the most under it. Quite simply, the strongest predictor of medical debt is the prevalence of illness. Indeed, US counties with the highest share of residents with multiple chronic conditions, such as diabetes and heart disease, tend to have accumulated the most medical debt. That makes illness a stronger predictor of medical debt than either poverty or insurance. This system also exacerbates racial disparities in health and medical care as well, with Blacks 50% more likely and Hispanics 35% more likely than whites to owe money for care. My cancer center is home to an excellent Population Studies and Disparities Program; so I have been aware of racial and socioeconomic disparities in cancer outcomes and burden for quite some time, having increasingly appreciated the issue over the 14 years since I accepted my current employment. I now therefore argue that understanding disparities in SBM care and how to eliminate them is part of SBM.

This brings me to one area for change and improvement. Certainly, there are other needed changes to make SBM more available to all, but I’m going to start with this one.

Health insurance and the pandemic

The story that I just discussed includes this quote:

“The No. 1 reason, and the No. 2, 3, and 4 reasons, that people go into medical debt is they don’t have the money,” said Alan Cohen, a co-founder of insurer Centivo who has worked in health benefits for more than 30 years. “It’s not complicated.”

Put this way, the reason for the problem might not be complicated, but the solution is. Again, this is where the interface between SBM and society gets messy. Still, let’s look to a PNAS study published a week ago by a group led by the Center for Infectious Disease Modeling and Analysis, Yale School of Public Health, and including investigators from the University of Florida, University of Massachusetts, Amherst, and Syracuse University. The study asked the question: What would the effect of universal health insurance have been on mortality in the US from the pandemic? Its conclusion is that universal health insurance is pandemic preparedness, and it concludes that ~212K who died of COVID-19 could have been saved in 2020 alone and that, overall, from the pandemic’s beginning until mid-March 2022, universal health care could have saved more than 338K lives from COVID-19 alone. In addition, the study estimates that single payer universal health care would also have saved the US government roughly $106 billion in health care costs associated with hospitalizations from COVID-19—plus an estimated $438 billion that could be saved in a nonpandemic year.

The methodology of the study was as follows. The authors calculated elevated mortality attributable to loss of employer-sponsored insurance and to background rates of being uninsured, summing with increased COVID-19 mortality attributable to low insurance coverage. Demographics and age-specific mortality rates due to COVID-19 were estimated, as well as prepandemic mortality, leading the authors to estimate that 338K deaths from COVID-19 alone could have been prevented over the two year period from March 2020 to March 2022. They then argue that Medicare-For-All could have saved these lives through a combination of:

- Improved access to primary care and reduction in comorbidities.

- Early diagnosis and access to life-saving medical care.

- Facilitation of COVID-19 preventative measures (e.g., vaccination).

- Alleviating pressure on hospitals during a pandemic.

There’s a large evidence base supporting the conclusion that health outcomes tend to be better with universal health care. However, I tend to agree with this analysis by Dylan Scott that points out a number of issues with the study above, not the least of which is its assumption that a single-payer universal health care system is the be-all and end-all of systemic solutions for improving health outcomes, decreasing disparities, and eliminating medical debt. For instance, it is very much true that COVID-19-associated mortality was very high in the US. We have 4% of the world’s population, but suffered 16% of the mortality burden due to COVID-19. It is also true that COVID-19 mortality was lower in countries with universal health insurance, in some cases a lot lower. However, there is the outlier of the UK, which, despite having single-payer universal health care (in the form of the National Health Service, or NHS), had a COVID-19 mortality rate almost as bad as the US.

Also:

All of these countries do have universal health care, but they do not all have a single-payer system in the vein of Sanders’s Medicare-for-all proposal. Taiwan does. But Australia utilizes a hybrid program where some people depend on public health insurance and other people use private plans. The Netherlands and Germany rely on private health insurance, heavily regulated and subsidized by the government. The UK’s National Health Service goes beyond single-payer and is fully socialized: The government not only pays for care for everyone but also runs hospitals and employs doctors directly.

I’ve often said elsewhere that universal health insurance does not have to be single-payer to be effective, and that was the main thing that irritated me about this Yale study; it assumed that only Medicare-For-All would be the answer to save all these lives from COVID-19, an assertion that it did not back up with evidence, mainly because it didn’t really seriously consider or compare other universal health insurance systems. (Also, one notes that even Medicare, which was examined in this study, only covers 80% of costs—after the deductible is met—unless one gets a Medigap policy or signs up for a Medicare Advantage plan.) Germany, for instance, has one of the oldest universal health insurance systems that dates back to the 1880s and survived the Nazi regime. It is what’s called a universal multi-payer health care system and encompasses both statutory health insurance for people who earn less than a certain salary, as well as private health insurance for those who earn more and choose to purchase their own. Moreover, clearly there have been other factors besides just universal health insurance.

As Scott notes:

Other factors might be in play beyond the specific type of health care system. As Damien Cave wrote for the New York Times in Australia, social trust seems to have been a decisive difference between the American and Australian experiences during the pandemic. The two nations share a lot of sociocultural DNA, but Aussies have much deeper trust in people in general, and their health care system specifically, than Americans do, Cave wrote. When I was reporting on South Korea’s successful Covid-19 response, Korean sources pointed in part to people there having a generally high level of trust in the government.

This also makes some intuitive sense. It follows that people in societies with more trust would be more likely to wear masks or stay home or get vaccinated not only for their own benefit but for the health of the people around them and society at large.

This brings us to the final point. SBM alone is not enough.

SBM versus values and politics

I’ve lost track of how many times when, as I discussed potential randomized controlled clinical trials (RCTs), I pointed out that sometimes the key value of SBM, namely doing best science possible to determine if a treatment works (a double-blind, placebo-controlled RCT) is not always possible because it conflicts with another value, specifically values of fairness and clinical equipoise as laid down by medical ethics. For example, I’ve long pointed out how doing a double-blind placebo-controlled RCT of the childhood vaccination schedule in the form of a “vaxxed/unvaxxed” study that some antivaxxers have periodically called for to “prove” that vaccines cause autism would be completely unethical because it would leave the control group unprotected against common childhood diseases. As a result, we have to rely on epidemiological studies to show that vaccines are not associated with autism.

The same principle operates on a much larger scale when it comes to a country’s willingness to institute public policies designed to bring SBM to as many people as possible, as Scott points out quite well:

Universal health care is a choice, a reflection of a country’s values. When reporting the Everybody Covered series, I found this quote from Princeton health care economist Uwe Reinhardt. It was in his most recent book Priced Out, which was published after he died in 2017:

Canada and virtually all European and Asian developed nations have reached, decades ago, a political consensus to treat health care as a social good.

By contrast, we in the United States have never reached a politically dominant consensus on the issue.

While traveling in Taiwan or the Netherlands, people would ask me about US health care and I would have to tell them that millions of Americans were uninsured and that people could be charged thousands of dollars for medical care. That was unfathomable to the people I met. They lived in a country where people agreed such things should never be allowed to happen.

America has never made that collective commitment to providing everyone with health care. The country paid the price for that shortsightedness during the pandemic, as this new study helps demonstrate. Whatever form it took, a universal health system would have likely prevented tens of thousands of deaths from the novel coronavirus.

As important as demonstrating how harmful medicine based on bad science and pseudoscience has been to patients and to the healthcare system in general, as well as how it has degraded standards of evidence in a manner that (I argued) facilitated the promotion of, for example, ivermectin as a miracle treatment for COVID-19, SBM in isolation is not enough. The system in which SBM is utilized is part of SBM, for better or worse. It can’t be repeated enough that SBM is much less useful if people can’t access it or the cost of accessing it is prohibitive. I’m therefore coming to the conclusion that not only is SBM necessarily political, it must be political, in order to find ways to change the dominant values in our political system in order to spark change that allows SBM to be accessible to all without ruinous cost. Unfortunately, these days we seem to be going in the wrong direction.